Gaap Depreciable Life Of Solar Panels

Week 4 Cfa Level Ii Key Differences Between Us Gaap And Ifrs Part I Youtube Cpa Exam Accounting Financial Ratio

20 2 Financial Reporting Considerations Related To Covid 19 And An Economic Downturn March 25 2020 Last Updated September 18 2020 Dart Deloitte Accounting Research Tool

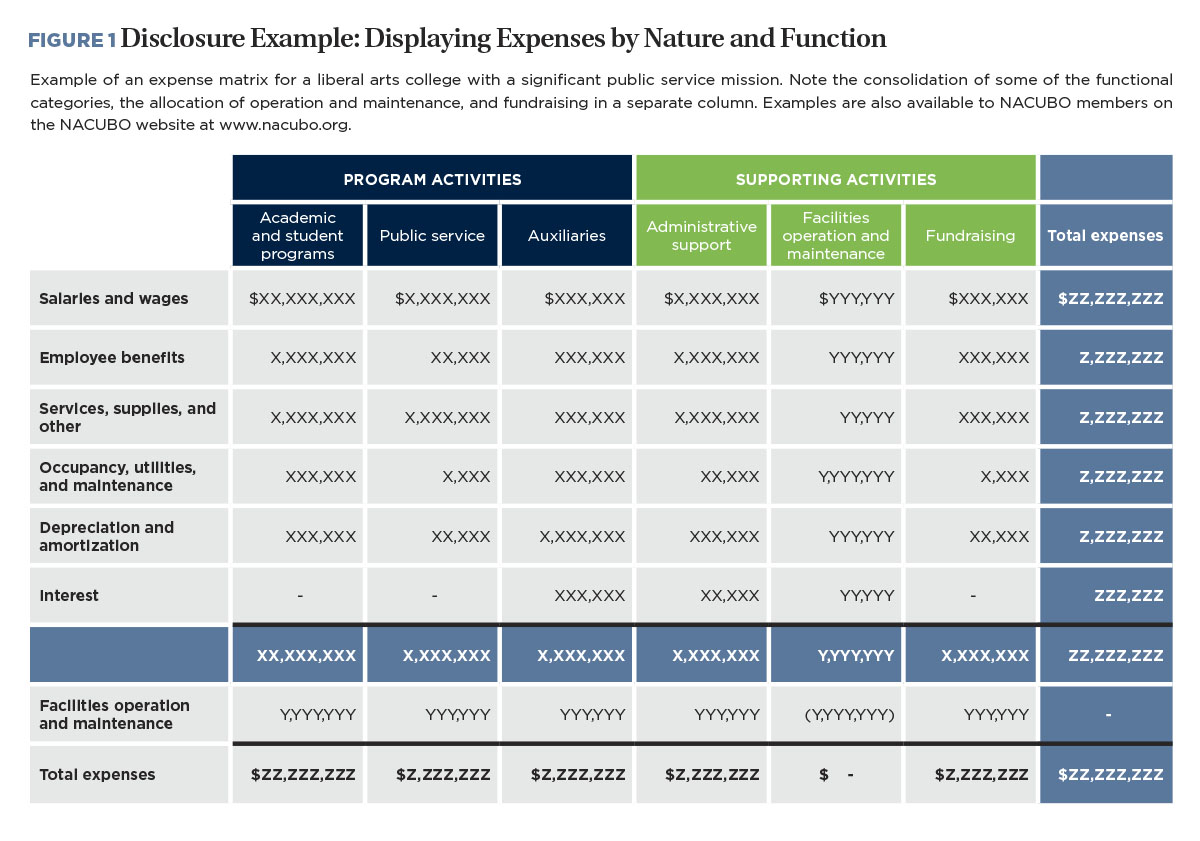

Putting New Rules Into Practice Business Officer Magazine

Pdf Big Gaap Little Gaap Will The Debate Never End

Types Of Accounting Accounting Government Accounting Cost Accounting

Solved Stellar Bright Solar Sbs Or The Company Is A B Chegg Com

Had sufficient amounts at risk under sec.

Gaap depreciable life of solar panels.

Ifrs Vs Gaap

Accounting Practitioners Guide For Renewable Energy Projects Pdf Free Download

Us Gaap And Ifrs Accounting And Reporting Issues For Shipping Companies Reminders And Updates Pdf Free Download

Fasb Issues Update To Insurance Accounting Standard Blog Deloitte Us

2019 Governmental Gaap Update Ppt Download

Tax Equity 201 Partnership Flips In Detail Woodlawn Associates

Ex 99 3

Does Convergence Of Accounting Standards Lead To The Convergence Of Accounting Practices A Study From China Sciencedirect

Ed20171231ex992

Ex 99 1 2 A18 40031 1ex99d1 Htm Ex 99 1 Exhibit 99 1 Q3 2018 Investor Presentation Forward Looking Statements And Non Gaap Financial Measures This Presentation Contains Forward Looking Statements That Reflect Our Current Views With Respect To

Ex 99 1

Sec Filing Mks Instruments Inc

Plot Land For Sale 200 0 Sq Yards In Near Mucharla And Karthal Srisailam Highway 12 3 Lakhs This Plot Is Government Approved Plo Land For Sale Layout Plots

Gasb Update Lisa R Parker Cpa Cgma Project Manager Ppt Download

Ex 99 1 2 T1701508 Ex99 1 Htm Exhibit 99 1 Exhibit

Elite And Premiere Guide Elite Guidelite Beachbody Coach Elite Beachbody 2019 Beachbody Coach Training Beachbody Coach Beachbody Workout Program

Investor Presentation Dated July 30 2020

Exhibit 99 2

Ex 99 1 2 A18 39566 1ex99d1 Htm Ex 99 1 Exhibit 99 1 Baird 2018 Global Industrial Conference November 6 2018 Mark C Jaksich Evp Chief Financial Officer Stephen G Kaniewski President Chief Executive Officer Graphic

U S Gaap From Basic Application To Current Topics Seminar August 31 September 1 B Purchase Accounting Under Gaap Ifrs Part I Advanced Pdf Free Download

Tagging Axis And Members Using The Us Gaap Taxonomy Guidance Xbrl Us

An28594426 Ex99 1 Htm

An Analysis Of The New Sale And Leaseback Guidance The Cpa Journal

Ex 99 1

Oil Sands

Ex 99 2

A4q2018earningsreleasepr

Ex 99 1

Fcel Ex992 32 Pptx Htm

Ex 99 1 2 A18 21048 1ex99d1 Htm Ex 99 1 Exhibit 99 1 Q2 18 Investor Presentation 1 Graphic Forward Looking Statements And Non Gaap Financial Measures This Presentation Contains Forward Looking Statements Within The Meaning Of Section 27a Of

Ex 99 1

Https Checkpointlearning Thomsonreuters Com Courses Filedownload Courseidhiddenfield 11666 Deliveryformatidhiddenfield 5

Ex 99 1

Insights Into Ifrs Lease Accounting Pdf Free Download

Ex 99 1

How Impending Fasb Changes Affect Your Real Estate Knowledge Leader Colliers Commercial Real Estate Blogknowledge Leader Colliers Commercial Real Estate Blog

Ex 99 2

Bloomenergyq219sharehold

Ex 99 1 2 Dp95306 Ex9901 Htm Exhibit 99 1 Exhibit

Advanced Energy Industries Inc 2020 Definitive Proxy Statement Def 14a

424b4 1 S002654x13 424b4 Htm 424b4 Table

A3q2018earningsreleasepr

Lettertoshareholderdated

Eva 8k Enviva Partners Lp Regulation Fd Disclosure Financial Statements And Exhibits August 11 2020

Source : pinterest.com